QuantFactory – Become A Quant Trader Bundle Download

Master Algorithmic Trading with Python and Build Your Own Profitable Trading Bots

Learn How To Develop, Backtest, and Optimize Profitable Trading Strategies

Unlock Your Financial Fredom Now!

——–

My name is Lachezar “Luke”, Co-founder of QuantFactory, and also a seasoned algorithmic trader with years of experience in the field.

You would want to listen to me because:

-

I’ve worked for top-tier quant hedge funds, where they only hire the best.

-

I’ve crafted more than 35 trading strategies that actually make money.

-

My trading bots are out there making profits as you read this.

-

I’ve developed over 350 different projects ranging from backtesting strategies and stock screeners to alert systems and deploying trading bots.

Now, I’m on a mission to deliver the MOST VALUABLE and PRECIOUS knowledge I possess, straight into your hands. I will be your guide, mentor, and ally on your path to becoming a successful quantitative trader.

——–

Two courses that are carefully crafted to take you from the fundamentals to the advanced concepts in quantitative finance and algorithmic trading.

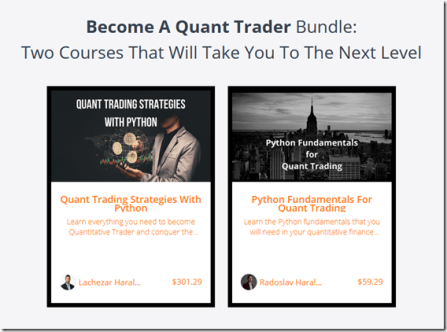

1. “Python Fundamentals For Quant Trading” – Beginner

This course is for all of you without experience in Python. You will learn the Python fundamentals and familiarize with the packages and libraries that you are going to use on a day-to-day basis.

2. “Quant Trading Strategies With Python” – Advanced

In the second course is where we get our hands real dirty. You will learn how to craft trading strategies that make sense. Where to find highly valuable resources and the data that you will need for your projects. You will learn how to develop an idea into code and backtest it on historical data. Then you will learn how to optimize it and perform an out-of-sample test.